From Here to Eternity

The crazy investments into AI infrastructure are based on a dangerously thin assumption. Here's why.

The majority is arguing about AI. They are arguing about the wrong thing.

On one side you’ve got the doomers, painting it all black. AI takes the jobs, then takes the economy down with them.

On the other side you’ve got the optimists. Their pitch: AI hands us scientific breakthroughs and a whole new wave of jobs. Marc Andreessen, one of them, calls the technology “the civilization-level multiplier”.

Underneath the debate there’s something more interesting, and a lot scarier. An intricate interplay between Big Tech, the AI labs, and the companies that make the chips. Together they fund the AI engine. And that engine is what’s been driving S&P 500 growth.

The whole machine runs on one big assumption: if you spend more, scale up the compute, eventually you’ll get an AI powerful enough to replace chunks of the workforce. That’s the one payoff big enough to justify all the money going in.

But what if this assumption is flawed?

As Benedict Evans said on a recent Lenny’s podcast:

“Are we going to get to human level of intelligence? Maybe yes, maybe not”.

It’s essentially a coin flip prediction.

Here’s why it’s a dangerous one.

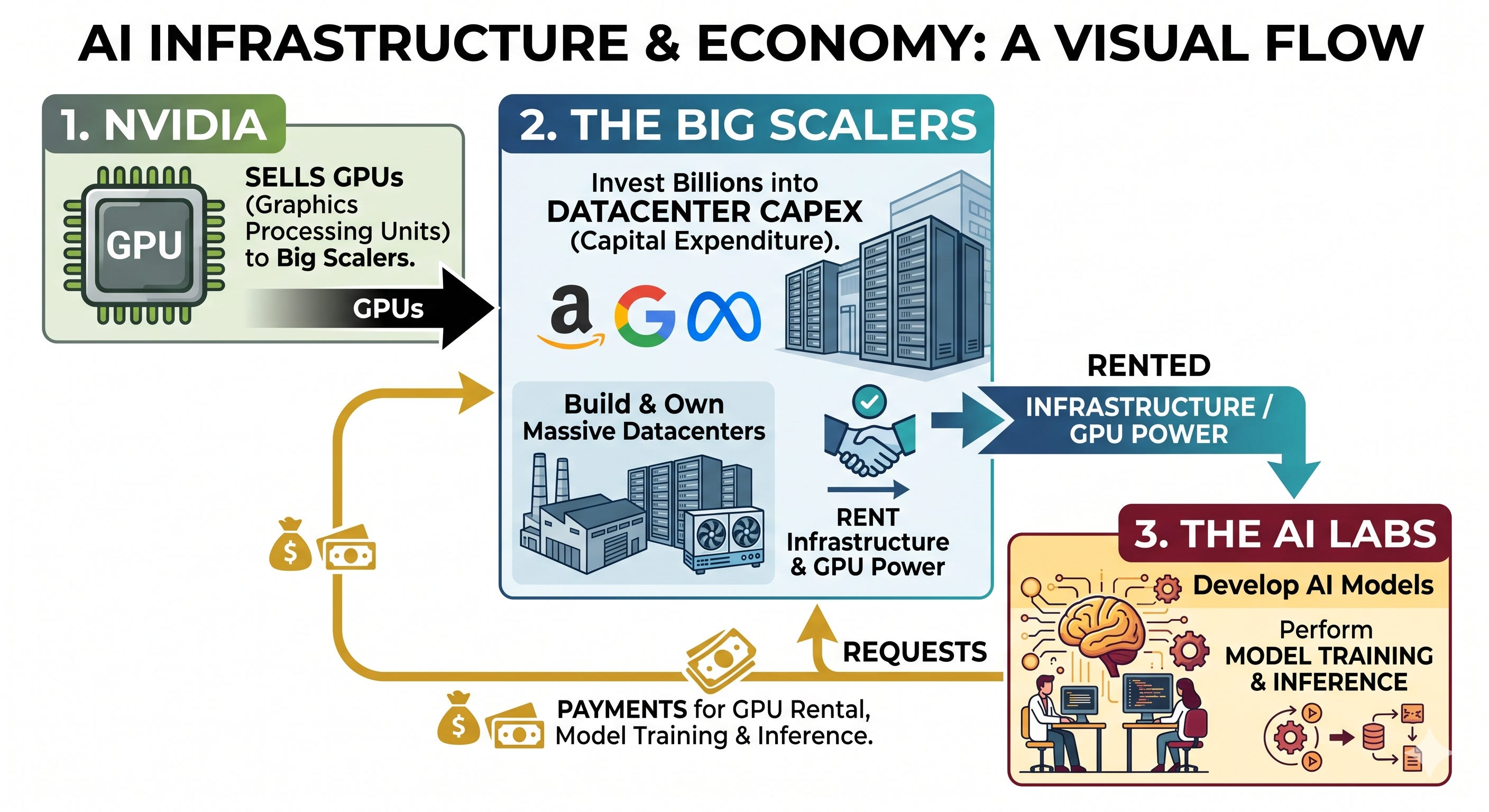

🌐 The AI Ecosystem

Nvidia. Manufactures and sells GPU chips to the Big Scalers.

The Big Scalers. Amazon, Google, Meta. They invest in datacenter capex, buy GPUs from Nvidia and rent the computing power to the AI Labs.

The AI Labs. Rent GPUs from the big scalers and pay for model training and inference.

🏗️ The Big Scalers

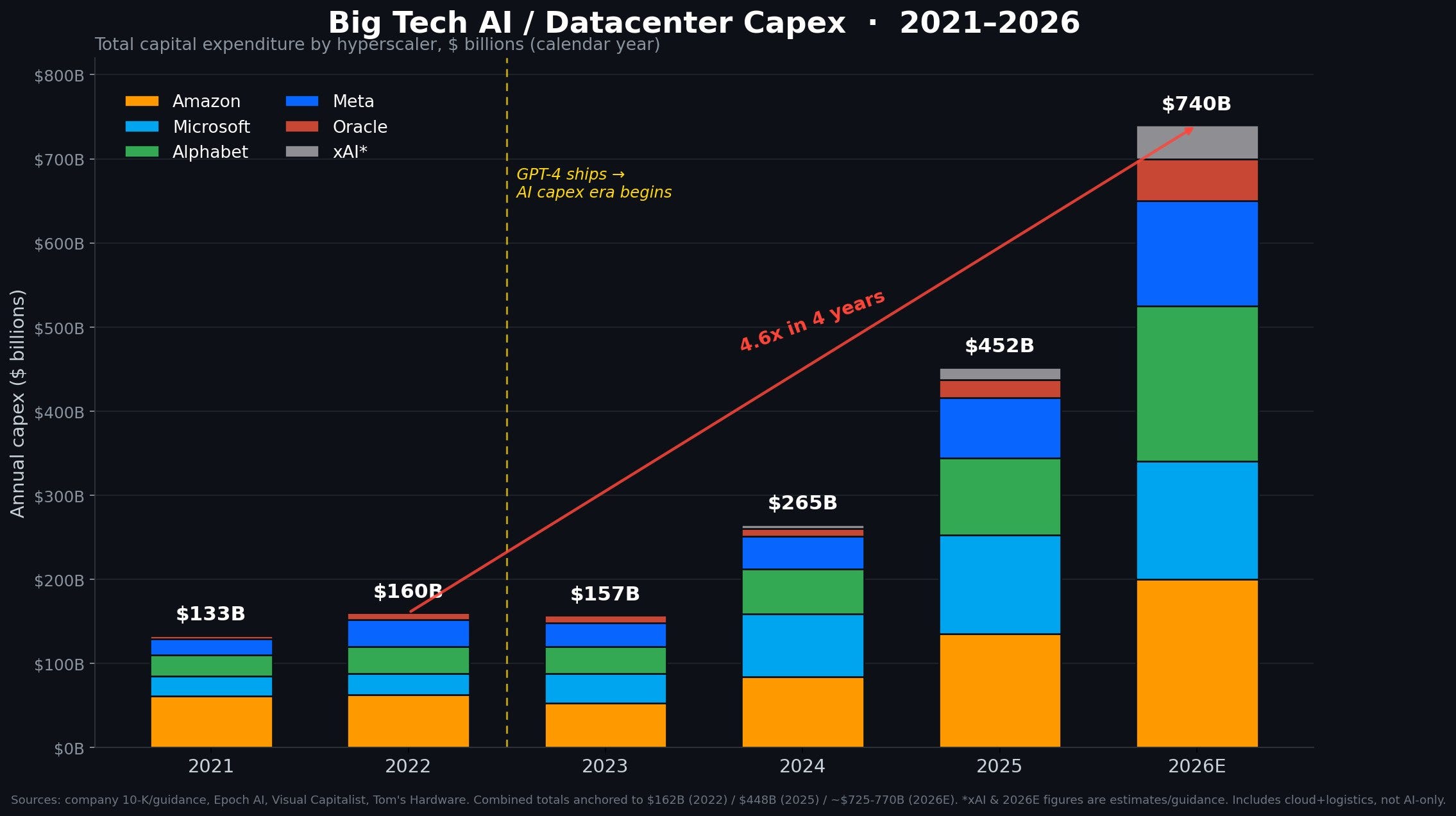

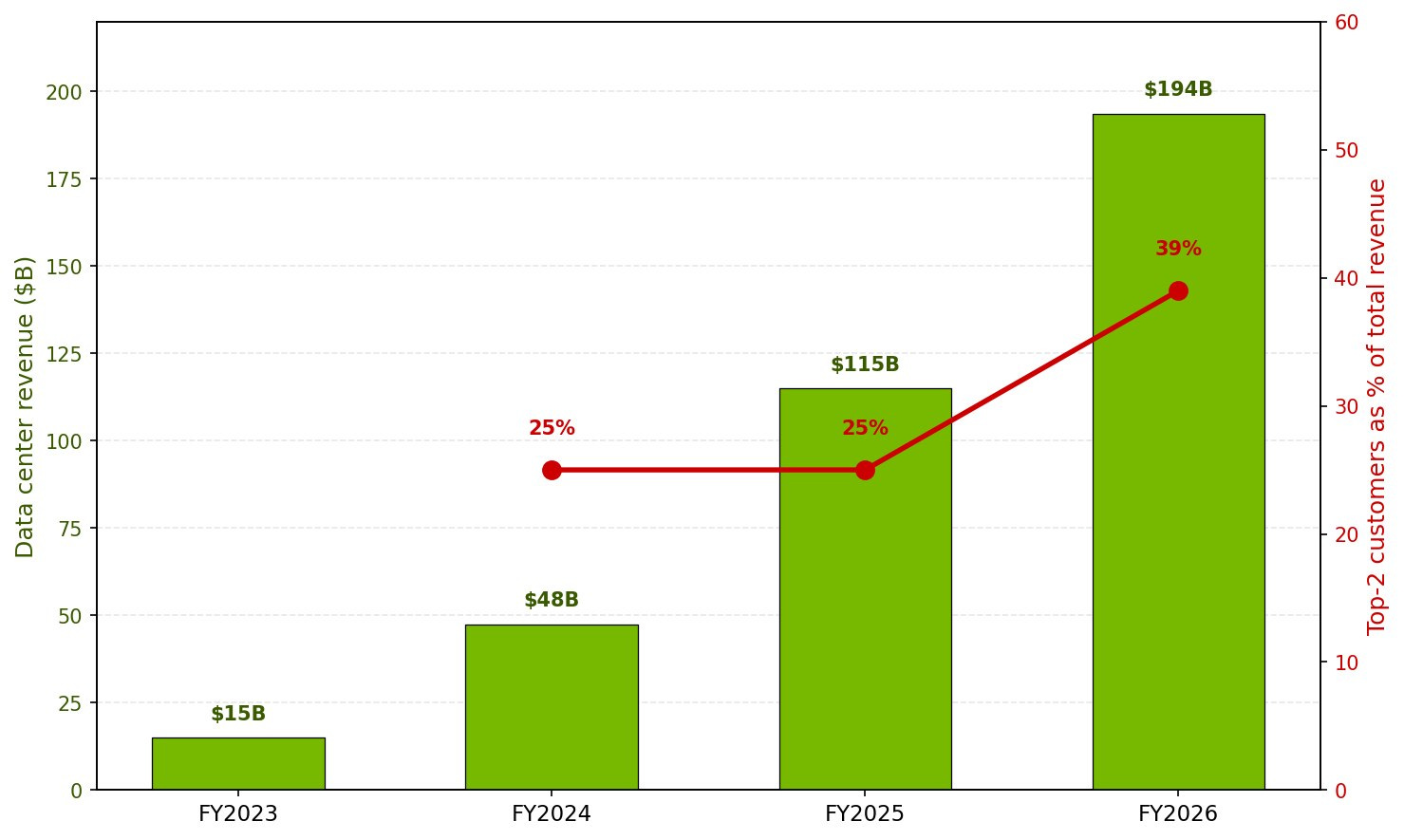

Datacenter investment has exploded - up 4.6x in three years, from $160b in 2023 to $740b in 2026.

First, about 20% of that spend (~$140b) is plain cloud compute, the AWS type of business. That part is solid: roughly $100b a year in revenue at 35%-plus margins. Sustainable business.

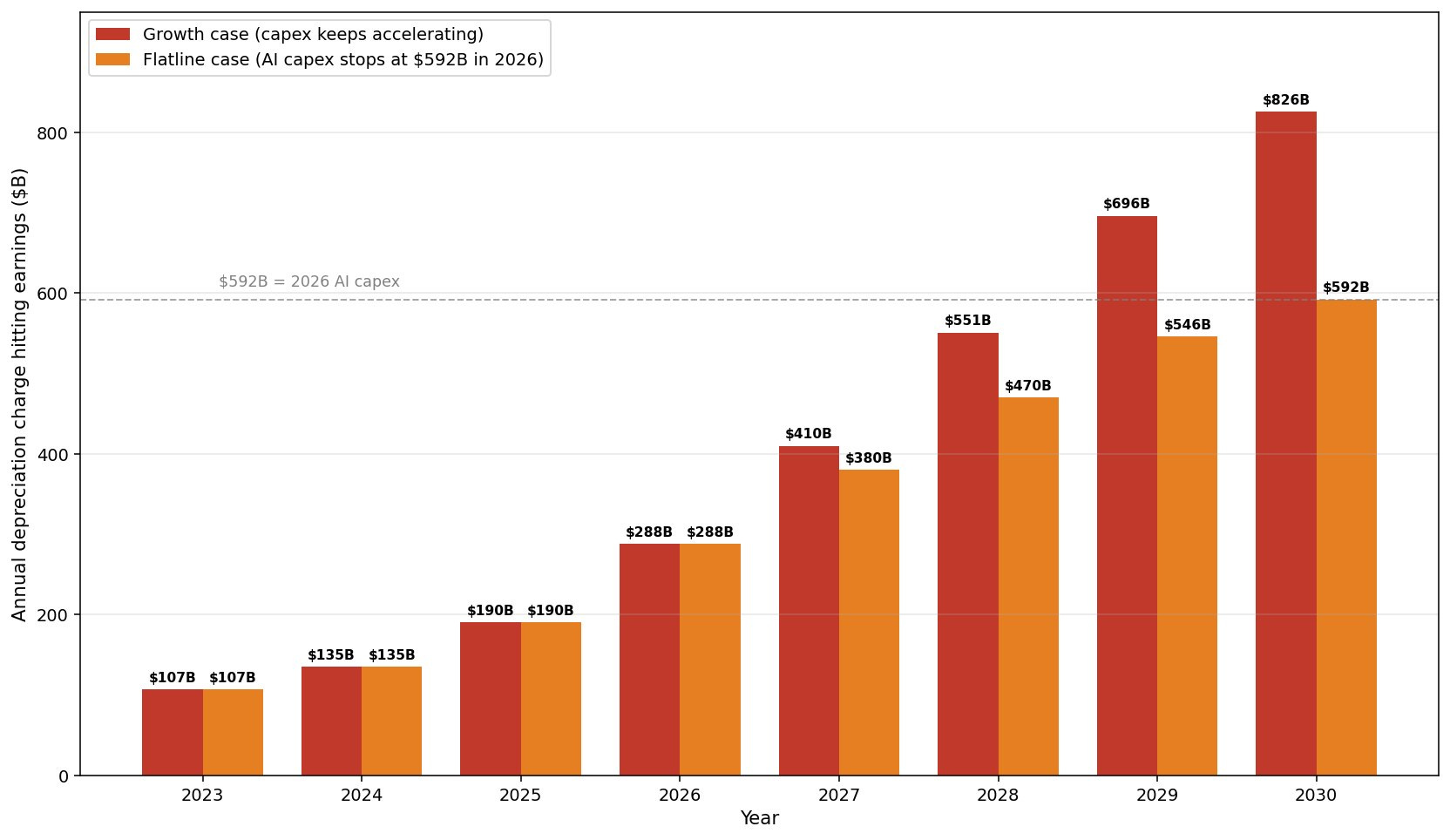

Second, data centers are a capital expense, so their cost gets depreciated over a lifetime of about 5 years. The cash leaves now, but only 20% of it lands on the books this year. The other 80% gets spread across the remaining four.

Here’s the catch, though: those charges pile up year after year. By 2026 Big Tech already has to book roughly $288b in depreciation. If the spending keeps climbing, that number reaches as high as $826b.

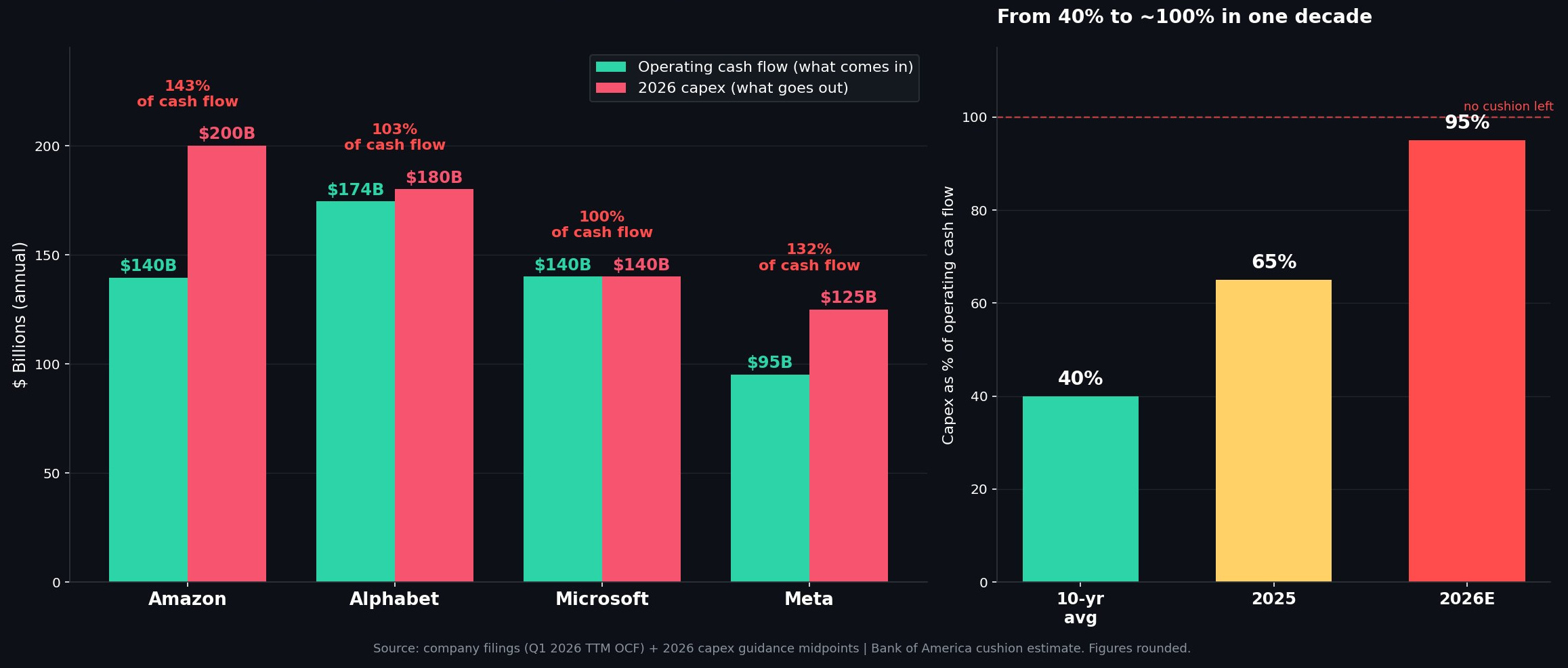

Third, and this is the tender spot of the whole thing, Big Tech is stretched thin actually covering those costs.

From 2015 to 2025, about 40% of their cash went into capex on average. That crept up to ~65% in 2025, then spiked to a scary ~95% in 2026.

To fund that, they’ve are going overboard. Meta and Amazon are now spending 32 to 43% more than cash they bring in. For every $1 of operating cash flow, they’re laying out $1.32 to $1.43 on capex.

To cover the gap they either dip into reserves (Amazon sits on $102b in cash plus $41b in securities, Meta on ~$23b plus $58b) or borrow it (Meta floated ~$30b in bonds to do exactly that).

Run a simple scenario where cash stays flat, and Amazon drains its reserves in about 2.4 years, Meta in roughly 2.7.

But their cash flow keeps growing with the core business, they can take on far more debt, and above all they can cut the capex any time they want. It’s an aggressive bet. It’s also an entirely voluntary one.

🧪 The AI Labs

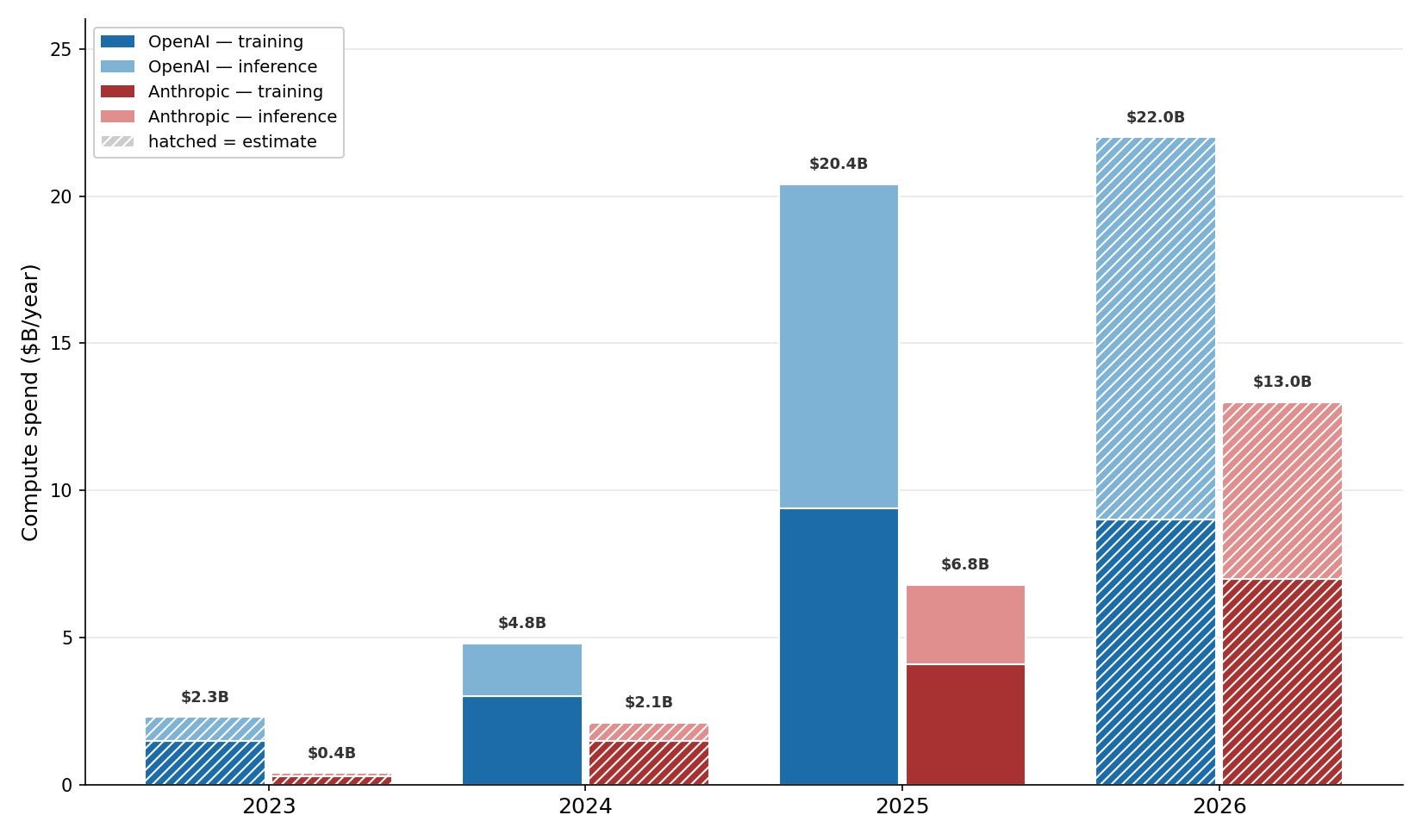

Let’s take two core labs (OpenAI and Anthropic) as the frontrunners.

OpenAI spent ~$20.4b on training and inference in 2025; Anthropic, around $6.8b (about $4.1b on training and $2.7b on inference).

Training a single frontier model runs ~$500m to $1b today, something like an Opus 4.8, and projections push that toward $10b within two years. Training is a one-time cost per model, but the experiments leading up to it burn plenty of compute too.

Inference, by contrast, is an ongoing spend. It already makes up 55% of OpenAI’s spend and ~30 to 40% of Anthropic’s, and it climbs every year a model stays in production.

What the labs really do is rent GPUs from the Big Scalers. They pay in one of two ways: with cash they raised from investors, or with compute credits handed to them by those very same Scalers who own the data centers. Microsoft is deep into OpenAI; Amazon and Google into Anthropic. The money goes out and comes right back to the landlord.

⛏️ Nvidia

39% of Nvidia’s revenue is concentrated in two top customers.

Sit with that number for a second. The most valuable company on the planet, selling the most sought-after product on the planet, and almost four of every ten dollars it earns walk in through just two doors. Nvidia won’t disclose whose, but well, it’s not that big of a secret. Customer A was 23% of revenue last quarter, Customer B another 16%, and both keep climbing - a year earlier the same two were closer to 25% combined.

Those two customers are Big Scalers, stretching their cash to spend on data centers. Pull in the rest of the hyperscalers and roughly half of Nvidia’s data center revenue comes from four or five companies spending on one thing: AI capex they can switch off whenever they please.

What looks like a broad market is a turf split between four landowners. There’s no consumer tier underneath to cushion a bad quarter, no long tail of small buyers. If two customers pull back, you cannot replace 39% of your revenue with gamers buying graphics cards.

🎲 The Core Assumption

📈 The Scaling Laws

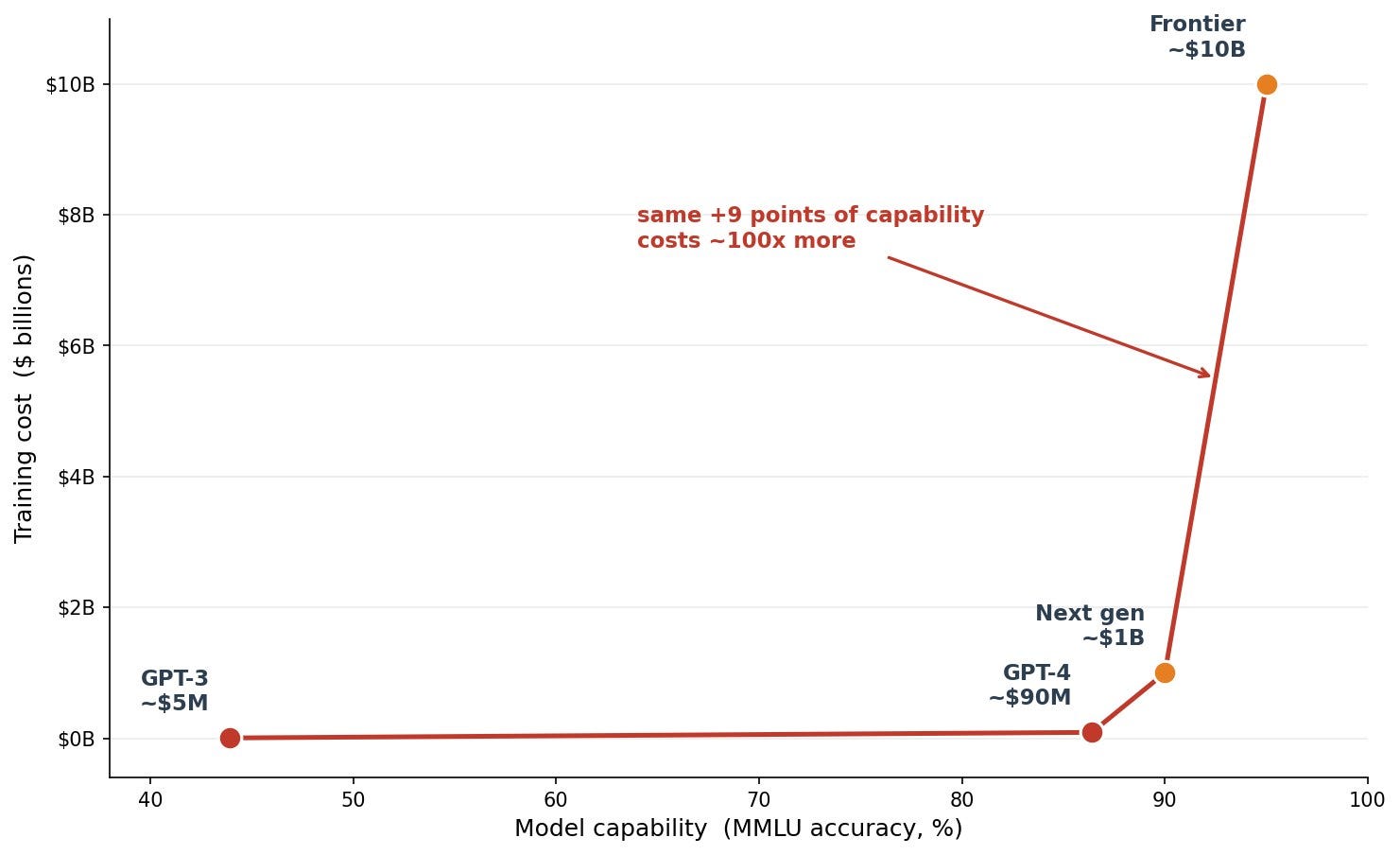

For years the recipe worked: pour in more compute, get a smarter model out. It held so consistently that it was coined as “a scaling law” and was treated practically like a law of physics.

The catch is that with scaling the model capability grows logarithmically (read marginally) while the costs spiral exponentially.

Going from GPT-3 to GPT-4 took about 70 times the compute and bought roughly 42 points on the standard knowledge test, from 44% up to 86%.

The next stretch, from 86% to 95%, takes another 20x the compute for just 9 more points. Every step costs exponentially more and yields way less.

GPT-3 cost around ~$5m to train. GPT-4, close to ~$90m. The next frontier model is projected near $1b, and the generation after that as high as $10b. That’s x100 the money just to squeeze out the final nine points of the scale.

📉 Compute Price Inflation

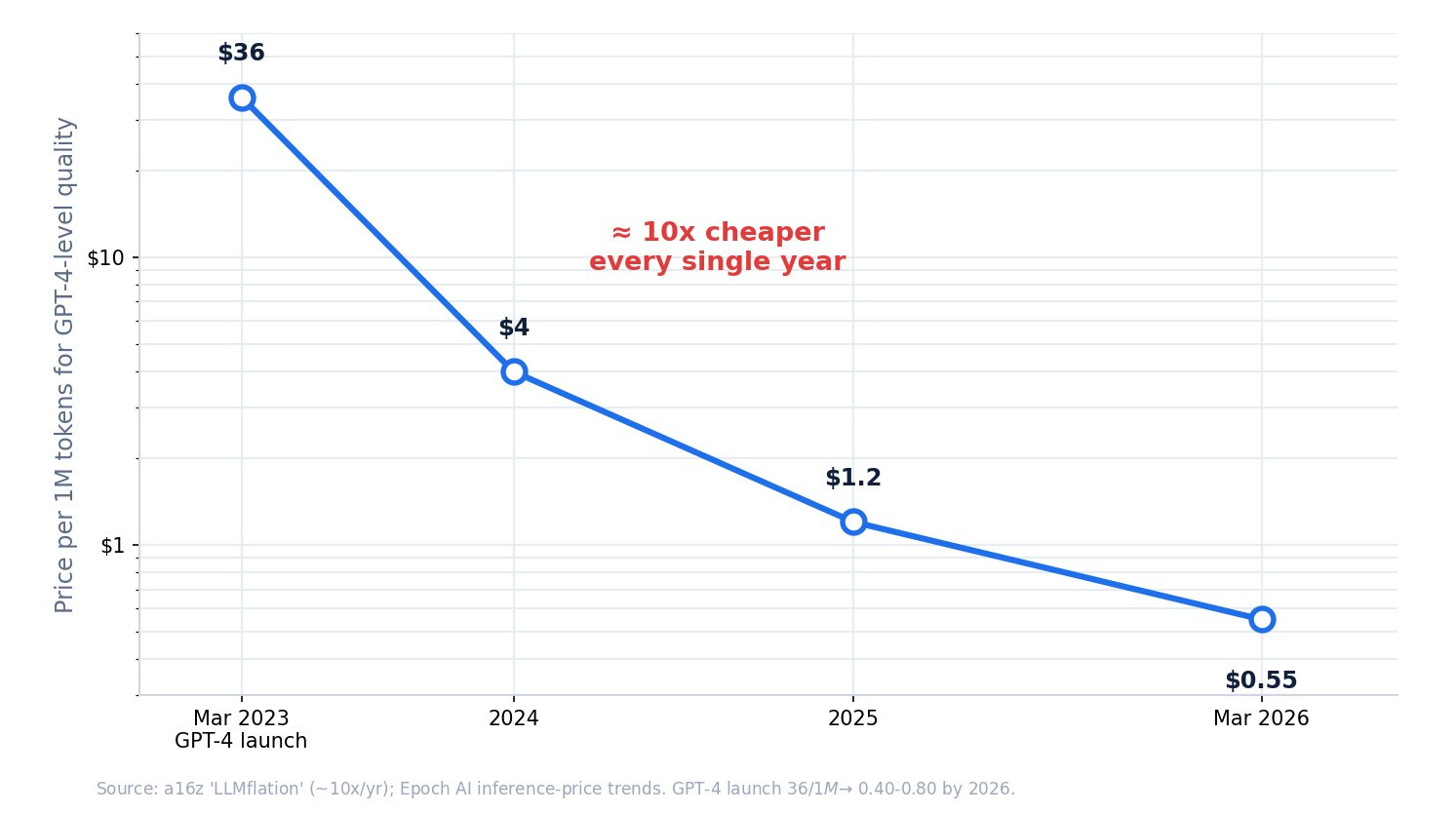

Now the second blade, working from the opposite direction. While the next model gets more expensive to build, the last model gets dramatically cheaper to run. The cost to serve any given level of capability falls by a factor of x10 every year. What was a frontier-grade product in 2024 is a commodity by 2026, and open-weight models give the same thing away for close to free.

a16z gave the effect a name: LLMflation. DeepSeek then poured fuel on it by training a competitive model for single-digit millions and releasing the weights for anyone to copy. The moment a capability becomes ordinary, its price falls toward the cost of the electricity it takes to run.

Put the two together and you have a core conflict. The next capability costs exponentially more; the last one earns almost nothing within a year. The only spot with real pricing power is the bleeding edge - and that’s exactly where the new reasoning models burn the most compute per answer. That’s the only place where AI Labs can charge a premium, albeit temporarily.

So the labs get squeezed from both sides at once. They pay an exponentially rising bill to build capabilities that drop to near-zero value inside a year. Only one prize is big enough to outrun that decay, and the whole trillion-dollar bet leans on it.

🐤 AI Replacing Workforce

So which payoff actually matters? It’s job replacement.

An AI that just helps a worker go faster gets commoditized to zero, like everything else on the LLMflation curve.

In contrast, an AI that removes the need to have a worker (and sheds a ~$70k annual salary off the corporate books) is the only payoff big enough to cover both the rising build cost and the rotting shelf life.

So it’s not really about the benchmarks or active usage. Benchmarks measure capability, user counts measure popularity. Neither tells you whether AI is replacing a salary or just sitting on top of it.

The real question: are companies hiring fewer people because the AI now does the work?

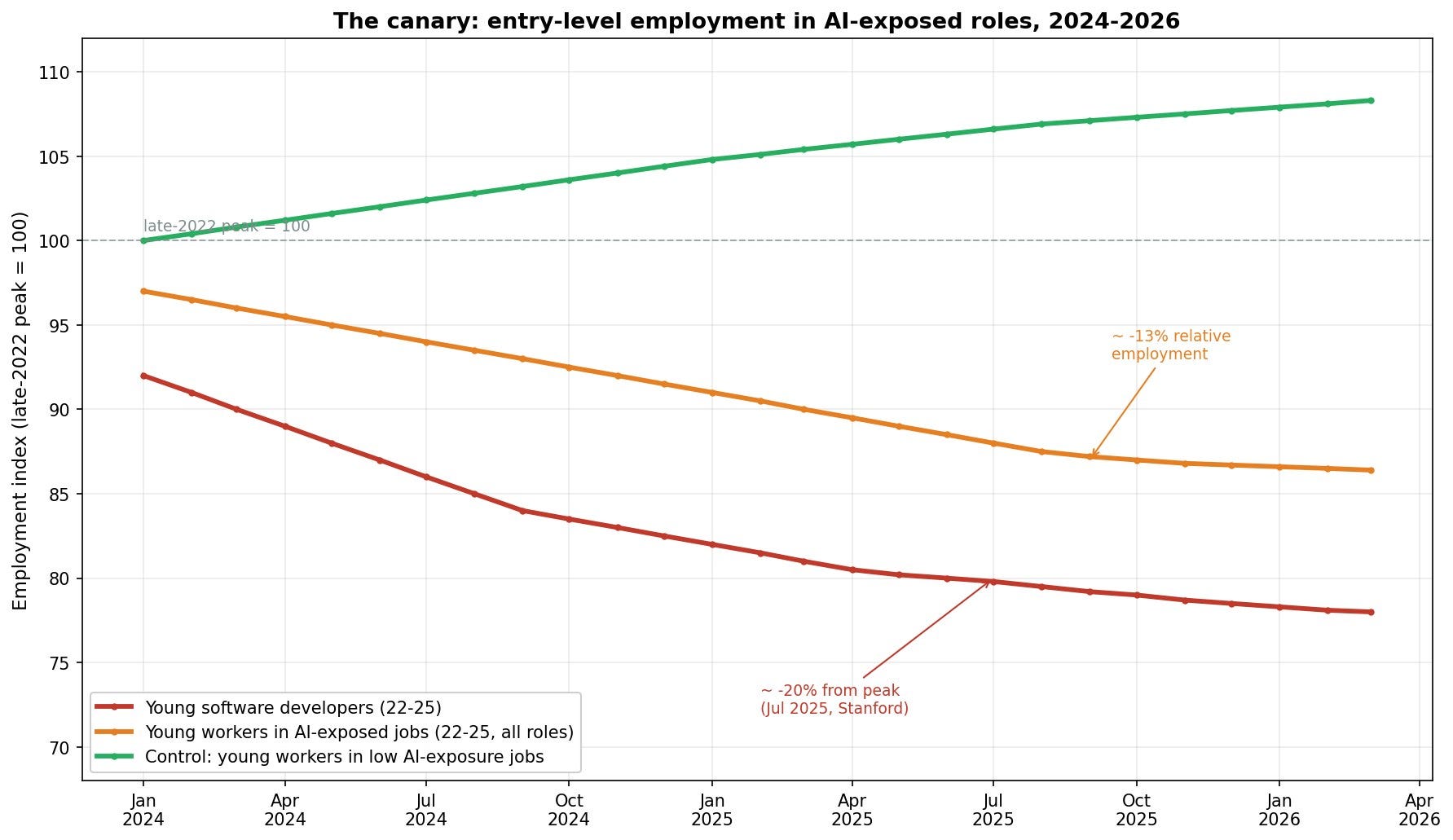

From the first glance at the statistics, it seems so. The entry-level white-collar jobs with high level of AI exposure are affected the most - the bottom rung of the chart shows that 22-25 year worker employment is down by -13% versus all other segments. The dataset is solid, it’s the real ADP payroll data on 25 mln workers, interpreted by Standford’s Digital Economy Lab.

But that’s a superficial view. Ultimately, ‘AI-exposed’ is a theoretical score and not a definite proof that companies are actually using AI instead of people. You can’t really decouple “AI took the jobs” from the “cheap money ended so we stopped overhiring”.

To sustain this, the AI Labs and BigTech desperately needs that -13% dip to be AI.

If we zoom out, what about the $600b capex cost question? To pay it off, how big should the dip be?

Now turn that into jobs. The datacenter build-out runs about ~$600b a year. To merely break even, the AI on top has to generate that much in real value; to actually profit, closer to double it.

Divide by what a worker costs - roughly $70k a year, fully loaded:

Just to break even: $600b ÷ $70k = ~8.6 million jobs.

To profit: $1.2t ÷ $70k = ~17 million jobs.

So the bet is to permanently erase somewhere between 9 and 17 million knowledge jobs. That’s roughly 10-15% of every desk job in the US. That number ballpark falls into the prediction I gave in one of my previous articles (The Corporate Collapse).

To be fair, no technology in history has ever reached that bar.

What if the bet doesn’t pay off?

Say the bet doesn’t pay. The other 50% of the coin flip probability.

More compute keeps buying less capability, the drop in entry-level hiring turns out to be the rate hangover instead of the robots, and the wage bill never falls. The spending stops making sense. So what breaks, in what order, and who would be the most affected?

The simplified view is that the bubble pops and everything cracks at once. The truth is messier, and the mess is the interesting part.

The labs fold fast; they run on rented compute and an assumption, and both evaporate (or get their R&D fully consumed by BigTech) the second the narrative cracks.

Nvidia’s next, because about 40% of its revenue is Big Tech capex. Nvidia won’t crumble, but the stock price is going to be significantly reevaluated, affecting the entire market.

Big Tech is affected the last, but they have the most immunity here. They will stop investing capex, take a writedown and continue focusing on their existing core businesses - be it E-commerce, Ads or Cloud. Their capex investment was always a bet in the first place.

Then there’s a second order effect on the stock market itself. All of the BigTech is going to take a hit on the market. They will fold AI and datacenter heavy projects, the spending will dry up, forcing deeper cuts, potentially driving the stock price further. What’s worse, since those BigTech players are the largest contributors to S&P growth (driving up to 40%), the index funds your pension is invested in (e.g. IWDA in EU) will be affected.

Note: None of this is a prediction. It’s just a map of what breaks if the core bet fails. One assumption is the fuse; everything above is the blast radius.

And it all comes down to a single question: can AI go from helping people work to doing the work itself? Until that’s answered, every chart in this piece is a live bet - and odds are you’re holding a piece of it without ever placing it.

🧾 TL;DR

The AI economy runs as a chain. Big Tech borrows and spends past its own cash flow to build data centers. Nvidia sells them the GPUs at a 75% margin and pulls 39% of its revenue from just two of those buyers.

The labs rent those GPUs back, often paying with money the same Big Tech companies handed them in the first place. And every link rests on one promise: that AI gets good enough to replace human work, not just speed it up.

That promise has a price. To break even, AI has to permanently erase somewhere around 12 to 15 million knowledge jobs, net of every job it creates. So far the data shows one young cohort slipping in one payroll dataset, and we can’t even prove that slip is AI rather than the end of cheap money.

If the promise holds, this will look like the cheapest trillion dollars anyone ever spent. If it breaks, the labs fold first, Nvidia reprices the same afternoon, Big Tech quietly stops digging and survives, and the stock market drags everyone down together, because underneath the six tickers it was always one bet.

The majority is still arguing about whether AI saves us or wrecks us. The real question is quieter, and it costs far more to get wrong: can the machine actually do your job? We don’t know yet. And until we do, every one of us owns a piece of that bet without ever placing it....

Misha, your article captures the core problem beautifully, but I think the truth is even scarier.

Even employee elimination is not a protected prize for AI labs. Even if AI can fully replace a worker in a given workflow, that can also be copied in a year, wrapped into cheaper models, and priced down toward commodity.

So the real moat is not “AI replaces people.” The moats are around the model distribution, workflow ownership, trust, compliance, integrations, data access, and liability.

But even most of those are not exclusive to AI labs either. Microsoft, Google, Salesforce, startups, and open-source ecosystems can replicate many of them once the capability is proven. Distribution and trust are harder to copy, but not impossible.

The question is whether AI labs not only could remove jobs, but also capture that fleeting value of job replacement before the replacement layer itself becomes just another cheap feature. And tbh I don’t have an answer to that.